Private Health Insurance Value Calculator

Is Private Health Insurance Right for You?

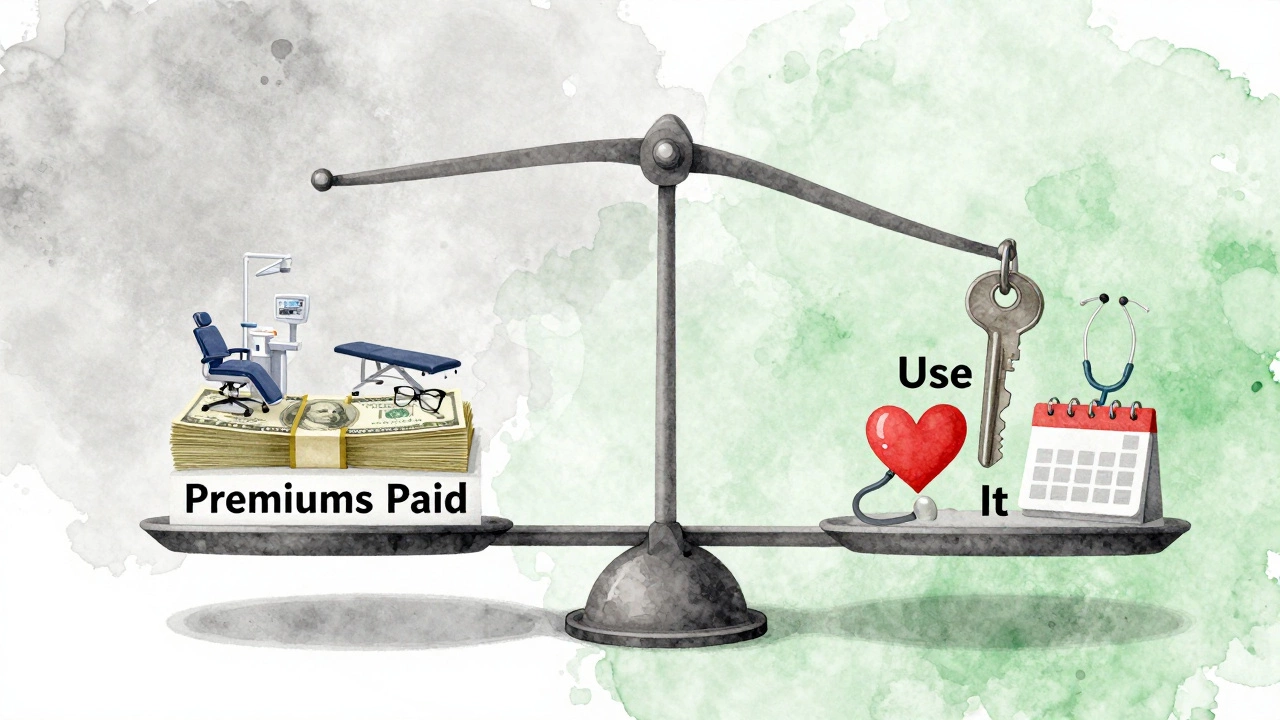

This calculator helps you determine if private health insurance makes financial sense based on your healthcare needs and usage patterns.

There’s no single "best" private health insurance in Australia. The right plan for you depends on your age, health needs, budget, and whether you care more about hospital cover or extras like dental and physio. What works for a 30-year-old runner might be useless for a 65-year-old with chronic knee pain. So instead of chasing a top-ranked plan, let’s cut through the noise and show you how to find the one that actually fits your life.

What private health insurance actually covers

Private health insurance in Australia breaks down into two main types: hospital cover and extras cover. Hospital cover lets you skip public hospital waiting lists and choose your own doctor. It pays for things like surgery, overnight stays, and specialist consultations in a private hospital. Extras cover is for everyday services that Medicare doesn’t touch-dentistry, optical, physio, chiropractic, and sometimes even acupuncture or podiatry.

Most people buy a combo plan. But here’s the catch: you don’t need both. If you’re young and healthy, you might only need hospital cover for emergencies. If you’re older and visit the dentist twice a year, extras might be worth more than your monthly premium.

Medicare covers basic public hospital care, but it doesn’t let you pick your surgeon or avoid long waits. Private insurance gives you control. But it’s not free. The average Australian pays between $100 and $200 a month for a mid-tier hospital and extras plan. That’s $1,200 to $2,400 a year. Is it worth it? Only if you use it.

How to compare hospital cover

Not all hospital policies are the same. Some cover heart surgery. Others don’t. Some let you go to any private hospital. Others restrict you to a network. Here’s what to look for:

- Exclusions: Check what’s not covered. Common exclusions include cosmetic surgery, fertility treatments, and some mental health services.

- Waiting periods: You can’t claim for pre-existing conditions right away. For most conditions, it’s 12 months. For psychiatric care, it’s often 2 months. Pregnancy is 12 months.

- Co-payments: Some insurers make you pay a set amount per day in hospital. Others don’t. This can add up fast.

- Choice of doctor: Does the policy let you pick your own specialist, or are you stuck with their panel?

For example, if you’re planning a knee replacement, make sure your policy covers orthopaedic surgery. If you’ve had back pain for years, check if spinal surgery is included. Don’t assume it is. Read the Product Disclosure Statement (PDS). No one reads it. But you should.

Extras cover: What’s actually useful

Extras cover sounds great until you realize you’re paying $50 a month for $300 a year in dental rebates. Most people don’t get their money’s worth. Here’s the truth:

- Dental: Basic check-ups and cleans are usually covered at 50-100%. Fillings? Often capped at $150-$200 per year. Root canals? Sometimes excluded or capped at $500. If you need major work, you’ll pay most of it out-of-pocket.

- Optical: Most plans give you $100-$250 every 1-2 years for glasses or contacts. If you need new lenses every year, that’s not enough.

- Physio: Usually capped at $50-$70 per session, with a yearly limit of $500-$1,000. That’s 7-14 visits. If you’re recovering from surgery or have chronic pain, you’ll need more.

- Chiropractic and podiatry: Often bundled with physio. Limits are low. Same deal.

Here’s a real example: Sarah, 42, pays $85/month for a plan with $1,000 annual extras cover. She gets two dental cleanings ($120), one eye exam ($100), and six physio sessions ($420). Total out-of-pocket after rebates: $180. She paid $1,020 for the year. She’s losing $840. That’s not insurance. That’s a bad deal.

Only buy extras if you use them regularly. If you go to the dentist once a year and never see a physio, skip it. Save the money.

Who gets the best value?

There’s no universal best insurer. But some do better for certain people:

- Young singles (under 30): Hospital cover only. Go for a basic policy with no extras. You’re unlikely to need much. Save money. Use the gap for gym memberships.

- Families with kids: Look for low waiting periods for pregnancy and paediatric dental. Bundled family plans can save up to 20% over individual policies.

- Seniors (65+): Focus on hospital cover for joint replacements, cataracts, and heart procedures. Extras matter less unless you wear dentures or glasses daily.

- Chronic condition sufferers: Check if your condition is covered. Some insurers exclude back pain, diabetes complications, or mental health aftercare. Read the fine print.

Medibank, HCF, Bupa, nib, and AHM are the big players. But smaller funds like Australian Unity and GU Health often have better value for specific needs. For example, GU Health offers unlimited physio for seniors on their top-tier plan. HCF has the lowest gap fees for orthopaedic surgery in NSW. You won’t find this on their homepage. You have to dig.

The hidden costs no one talks about

Insurance isn’t just about premiums. There are three sneaky costs:

- Annual limits: You hit your cap for dental or physio, and you pay the rest. That’s not a surprise-it’s standard.

- Gap fees: Even with hospital cover, your surgeon might charge more than the insurer pays. That’s the gap. Some insurers cover 100% of the Medicare Benefits Schedule (MBS) fee. Others only cover 75%. The difference comes out of your pocket.

- Loadings: If you sign up after 31, you pay a 2% loading per year for life. So if you wait until 40, you pay 18% extra. That’s not a discount. That’s a penalty.

And don’t forget the Lifetime Health Cover loading. If you don’t have hospital cover by July 1 after your 31st birthday, you pay more every year you delay. It stacks up. By 45, you could be paying 30% more than someone who signed up at 25.

What to do next

Stop scrolling through "Top 10" lists. They’re usually sponsored by the insurers themselves. Instead:

- Write down your last 12 months of healthcare spending: dentist visits, physio, prescriptions, hospital trips.

- Decide what you actually need. Do you need extras? Or just hospital cover?

- Go to the Private Health Insurance Ombudsman website. Use their comparison tool. Filter by your state, age, and needs.

- Call two insurers. Ask: "What’s the gap for a knee replacement?" and "What’s the annual cap for dental fillings?" Write down the answers.

- Compare the total cost: premium + expected out-of-pocket costs. Pick the lowest total.

Most people overpay because they buy what their friend has. Or they panic because they think they "need" everything. You don’t. You need what you use.

When private insurance isn’t worth it

There are times when private health insurance just doesn’t make sense:

- You’re under 30 and healthy. Use Medicare. Save your money.

- You’re on a low income. The government rebate is small. You’ll pay more in premiums than you get back.

- You rarely visit the doctor or dentist. You don’t need extras.

- You’re planning to leave Australia soon. No point paying for cover you won’t use.

Medicare covers 100% of public hospital costs. It covers bulk-billed GP visits. It covers essential medicines under the PBS. You don’t need private insurance to get basic care. You need it to avoid waiting lists and choose your doctor. If that doesn’t matter to you, skip it.

Final tip: Review your policy every year

Your needs change. So should your cover. Every November, ask yourself:

- Did I use my extras? How much did I get back?

- Did I have any hospital stays? Was the gap fee reasonable?

- Is my premium going up more than inflation?

If you didn’t use it, downgrade. If you kept hitting limits, upgrade. Don’t let your policy sit on autopilot. Most people pay $1,500 a year for coverage they never touch. That’s not smart. That’s wasted money.

The best private health insurance isn’t the most expensive. It’s the one you actually use. And you know what you need better than any salesperson.

Is private health insurance worth it in Australia?

It’s only worth it if you use it. If you regularly need hospital care, want to pick your doctor, or visit the dentist and physio often, then yes. If you’re young, healthy, and rarely see a doctor, Medicare is enough. Most people overpay because they buy extras they don’t use.

What’s the cheapest private health insurance in Australia?

The cheapest hospital-only cover starts around $40-$60 a month for a single person under 30. For extras, basic dental and optical plans start at $25-$40 a month. But cheap doesn’t mean good. A $30 plan might cap dental at $100 a year. That’s not coverage-it’s a joke. Look at total out-of-pocket cost, not just the premium.

Can I get private health insurance if I have a pre-existing condition?

Yes, but you’ll have to wait. For most conditions, the waiting period is 12 months. For psychiatric care, it’s usually 2 months. Pregnancy is 12 months. You can’t claim for the condition during that time. Some insurers exclude certain conditions entirely. Always check the PDS before signing up.

Do I need extras cover if I go to the dentist once a year?

If you only go for a check-up and clean, you might break even. Most plans cover 100% of basic dental, so you pay nothing out-of-pocket. But if your plan costs $60 a month, that’s $720 a year. You’re paying $720 to save $120. That’s not a win. Only get extras if you use them often-like needing fillings, crowns, or regular physio.

What happens if I cancel my private health insurance?

You lose your cover. If you rejoin later, you’ll pay a 2% loading for every year you were without hospital cover after turning 31. That loading sticks for life. So if you cancel at 35 and rejoin at 40, you’ll pay 10% extra on your premium forever. Also, you’ll have to serve new waiting periods for any conditions you develop while uninsured.

If you’re unsure, talk to a registered health insurance advisor. They’re paid by commission, so ask: "Which plan gives me the best value for my needs?" Not: "What’s the cheapest?"